If you’ve got a side hustle, you’re not alone. A few deliveries after work, some bits on Etsy, a spare room on Airbnb, the odd freelance job on Fiverr. Most people assume it’s too small to matter, or they’ll “sort it later”. The thing is, HMRC has much better visibility now. From January 2024, online platforms started sharing seller and host income data directly with HMRC. So rather than hoping it stays under the radar, the sensible approach is to make sure your reporting matches what’s been paid to you.

In this article we’ll go through which platforms this covers (think Uber Eats, Deliveroo, Etsy, eBay, Airbnb, Fiverr, Upwork and Amazon), how the £1,000 trading allowance works in real life, and when you actually need to register and do a tax return. We’ll also look at how side hustle income combines with your other income for Making Tax Digital thresholds (that’s HMRC’s move towards more frequent digital reporting), and what to do if you’ve already earned money and haven’t declared it yet. Most of the time it isn’t people being sneaky. It’s just that nobody told them the rules.

From January 2024, lots of the big online platforms started reporting income details to HMRC. In plain terms, if you get paid through an app or marketplace, the platform can pass on information about what you were paid and who you are.

This is the sort of thing that affects ordinary side hustles. Food delivery with Uber Eats or Deliveroo. Selling on Etsy or eBay. Hosting on Airbnb. Freelance jobs on Fiverr or Upwork. Even Amazon sales. It is not about whether you are a “business” in the traditional sense. It is about money moving through a platform that can now be reported.

The key shift is visibility. HMRC does a lot of “data matching”, which just means comparing what you declare on a tax return (or don’t declare) with what third parties report. Banks have been in that mix for years. Platforms are now part of it too.

To be honest, this is not designed to catch people out for an honest mistake. Most side hustlers are not trying to hide anything. They just do not realise that a few hundred here and a few hundred there is still income, and that the platform records are very tidy compared to your own back-of-the-phone-notes.

One practical point on timing: you might not hear anything straight away. Data matching can happen later, sometimes long after the tax year has ended. So the quiet period after you have had a good month on Deliveroo or a big run of Etsy orders does not really tell you much.

If you want a sensible approach, keep your own basic records now, even if you think you are under the £1,000 trading allowance. In practice, platforms can show sales and payouts, but they will not know your expenses. If HMRC ever asks a question, being able to explain the numbers calmly is usually half the battle.

If you’ve been paid through a platform, assume there’s a record of it that can be shared. The obvious ones people mention are Uber Eats and Deliveroo for delivery work, Etsy and eBay for selling, Airbnb for hosting, and Fiverr or Upwork for freelancing. Amazon comes up a lot too, especially for people doing small-scale reselling or Fulfilment by Amazon.

That list is not exhaustive. Other apps and marketplaces may also report, and new ones get added over time. So it’s better to think in categories rather than brands: if a platform takes the customer payment, pays you out, and has your details, it is capable of passing information to HMRC.

Also, not every platform reports in exactly the same way. Some will have cleaner data than others. And it is not safe to assume HMRC sees every individual transaction in real time. In practice, it tends to be summary-style information that helps HMRC cross-check whether you have declared the income at all.

It helps to separate what you are doing, because the tax treatment can differ. Selling goods is things like Etsy, eBay or Amazon. Providing services is the work you do, like deliveries for Uber Eats and Deliveroo, or freelance design and admin work via Fiverr or Upwork. Letting property is Airbnb, even if it is “just a spare room”. Those buckets matter because the expenses you can claim, and sometimes the forms you use, can be different.

A small judgement call here: if you are using more than one platform, do not rely on each app’s numbers to tell your story. Keep your own simple total of income paid out and the main costs (fees, mileage, materials, software). It takes half an hour a month, and it makes the tax side calmer later.

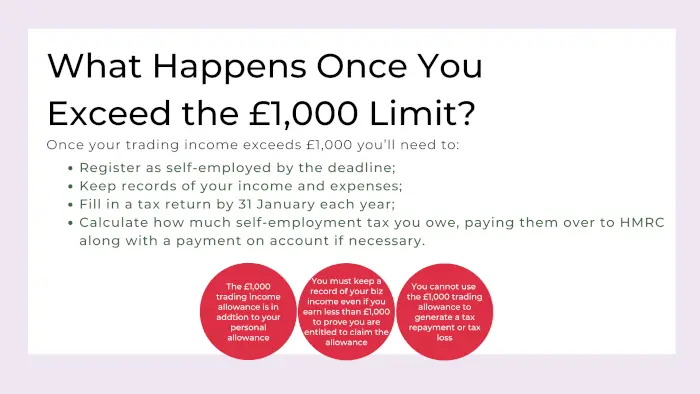

The £1,000 trading allowance is a simple rule that lets you earn up to £1,000 of gross trading income in a tax year, and in many cases you won’t need to report it. “Gross trading income” just means your total sales or fees before taking off any costs.

This is where people get caught out. They hear “£1,000” and think it is about profit. It isn’t. It is about turnover. Turnover is the money that comes in. Profit is what is left after costs like platform fees, postage, materials, mileage, phone bills, software, and so on.

Also, the allowance is not a free pass that guarantees you never need to register or file anything. Whether you need to do a tax return can depend on your wider situation, and on what other income you have. If you already do Self Assessment for another reason, for example, you still need to make sure the figures you report are correct.

There is another practical point people miss. If you use the £1,000 trading allowance, you usually give up the right to claim your actual expenses for that income. So sometimes it is better to declare the income anyway, because your real costs are higher than £1,000 and your taxable profit is lower as a result.

Example one: an Etsy seller has £1,200 of sales over the year and £500 of costs (postage, Etsy fees, packaging). They are over the £1,000 threshold on turnover, so it is not a “do nothing” situation. In practice you would normally declare it, and you would pay tax on the profit, which is £700, not on the £1,200.

Example two: a delivery rider has £900 of income. On the face of it, that is under the £1,000 trading allowance. But if they have high costs, like bike repairs, safety gear, and a decent chunk of phone and data used for work, the actual profit might be small. It can still be worth keeping records, because if you end up needing to file for another reason, or the side hustle grows, you do not want to be guessing later.

My small judgement call is this: if you are close to £1,000, or your costs are significant, track it properly from day one. A simple monthly note of income paid out and main expenses is enough. It gives you options, and it stops the tax side turning into a scramble next January.

“Register” usually means registering for Self Assessment, so you can submit a tax return. Self Assessment is simply the system where you tell HMRC what you earned in the tax year, what allowable costs you had, and what tax is due.

If your side hustle income is over the £1,000 trading allowance (remember, that is turnover, not profit), you normally move from “nice and simple” into “you probably need to report this properly”. In practice, that often means you register for Self Assessment and file a tax return for that tax year.

You may also need to register even if your side hustle is under £1,000, because Self Assessment is triggered by your wider situation too. Some people already file because they have rental income, they are a company director, they have untaxed income, or they have other reasons HMRC expects a return. If you are already in Self Assessment, you cannot just ignore a side income stream. It still needs to be included, even if it is small.

Another common trigger is having multiple income streams. Maybe you are on payroll Monday to Friday, then you do Deliveroo at weekends, sell on eBay, and pick up a bit of Fiverr work. Each one might feel minor. Added together, it can push you over the levels where reporting is needed, and it can also make it easier to miss something if you are not tracking it.

And then there is the “I want to claim expenses properly” trigger. If you use the £1,000 trading allowance, you usually do not claim your actual expenses for that income. If your costs are higher than £1,000, or you have a lot of costs that matter (platform fees, mileage, equipment, materials, postage), it can be more sensible to report the income and claim the real expenses instead. That is often where registering and filing becomes worthwhile, even when you are not massively over £1,000.

One quick way to think about it is this. If your side hustle turnover is over £1,000, assume you need to report it and check whether you need to register. If it is under £1,000, ask yourself two questions: am I already in Self Assessment for another reason, and would I be better off claiming my actual expenses? A “yes” to either means you should not just leave it.

Do not leave the admin until the last minute. Registering and filing are time-sensitive, and HMRC processes can be slower when lots of people are trying to do the same thing at once. My judgement call: if you are even slightly unsure, sort it early in the tax year after you start earning, not after Christmas when everyone suddenly remembers.

This is the bit that catches people out. If you have a PAYE job (a normal job where your employer deducts tax from your pay) and you also earn from a side hustle, HMRC looks at both together when working out your tax for the year.

So PAYE wages plus self-employed or side income equals your total taxable income. That total is what decides which tax band you fall into, and it can also affect things like Child Benefit charges for some people. I am not going to try and cover every rule here, but the basic stacking-up point matters.

A simple example. Say you earn £38,000 on salary and your tax through PAYE looks fine all year. Then you do Deliveroo at weekends and make £4,000 turnover, with some costs, and end up with (say) £2,500 profit. That £2,500 does not get taxed in isolation. It sits on top of your salary when HMRC does the final calculation, and you can end up owing extra tax at the year end through Self Assessment.

Same story if it is Fiverr or Upwork work in the evenings. The platform pays you, you get the money in your bank, and it feels done. But HMRC usually has not taken any tax at source on that income, so there is nothing stopping a bill building up quietly in the background.

That is why people get an “unexpected” tax bill. It is not a penalty. It is just the tax that was always due, but it was not collected month by month like your salary tax was.

In practice, my small judgement call is this: if your side hustle is more than pocket money, put a bit aside for tax as you go. It does not need to be perfect. Even parking 20-30% of the profit in a separate savings pot can stop January being a nasty surprise, especially if your PAYE income already uses up most of your basic rate band.

MTD for Income Tax (Making Tax Digital) is HMRC’s move towards digital record keeping. Instead of doing everything once a year, you keep your income and expense records in compatible software and send updates during the year, then do an end of year finalisation.

The bit most people miss is how the thresholds work. The test is based on your gross income from self-employment and property. Gross means before expenses. So your Uber Eats or Deliveroo takings, your Etsy or eBay sales, your Airbnb receipts, your Amazon marketplace turnover, your Fiverr or Upwork income – that sort of thing. If you also have rental income, that is in the same basket for this test.

Your PAYE job is usually not the thing that pushes you into MTD for Income Tax. In practice, it is the side business and property income that matter for MTD, even if your salary is your main income and the side hustle feels like a small add-on.

It can catch people who have a few different streams that each look harmless on their own. One platform account here, a room on Airbnb there, a bit of selling on Etsy at weekends. Add them together and you can edge towards the point where HMRC expects quarterly-style reporting.

A quick scenario. Someone hosts a spare room on Airbnb and it does fairly well in summer. They also run a small Etsy shop selling handmade prints. Neither one feels big. But when you add the Airbnb gross receipts to the Etsy gross sales, the total can creep up year by year, and you might suddenly find you are in scope for MTD when it comes in for you.

My judgement call: if you have more than one of these income streams, start keeping clean digital records now, even if you are not sure MTD applies to you yet. It is much easier to switch to proper tracking early than to try and rebuild a year of numbers from bank statements and platform downloads later.

When people hear “declare your income”, they often picture the money they had left over after a busy month. HMRC does not see it that way. In general, your income is the total you receive from the work or sales, before your personal spending.

One thing that trips people up is platform fees and commissions. Some platforms pay you after taking their cut. Others show you the “customer paid” amount, then show fees separately. In practice, you want to report it in a consistent way so your income and expenses make sense together. If you are not sure which figure is the right starting point, use the platform statements and we can sanity check it.

Then come the deductions. A deduction is just a cost that was genuinely for the business, not private life. You do not need to overthink it, but you do need to be able to explain it.

If you do delivery work (Uber Eats, Deliveroo and similar), the usual costs are mileage if you use a car, or running costs if you use a bike or e-bike. You may also have things like a phone and data (often a proportion, not the whole bill), protective gear, and replacement kit you need for the job. Keep it sensible. If you buy something that is half personal, half work, only claim the work part.

If you sell online (Etsy, eBay, Amazon), the everyday deductions tend to be materials, packaging, postage, and the platform fees. Payment processing fees usually count too. If you buy stock to resell, that is normally part of your cost of sales. Again, the key is evidence and a clean trail from purchase to sale.

If you freelance on Fiverr or Upwork, it is often software subscriptions, small equipment, and sometimes a fair home office proportion. “Home office” here means the extra cost of using your home for work, not your whole rent. A simple way is to use a reasonable split based on space and time used. Keep a note of how you worked it out so you can repeat it next year.

Airbnb is a bit more case by case, because it depends on your set-up. Renting out a room in your own home looks different to running a whole property as a short-let. There are usually allowable running costs, but you need to match them to what is actually being let, and whether any costs are partly personal. If you are using the place yourself as well, that usually means apportionments and a bit more care.

Records make this calmer. You do not need a finance department. Basic bookkeeping is enough: keep invoices and receipts, download platform statements, and make sure your bank transactions back it up. Bank feeds in accounting software help because they pull transactions in automatically, which cuts down the “where did that go?” problem later.

A quick warning, because it causes real headaches: mixing personal and business money makes life harder. When everything runs through one personal account, it is still workable, but you spend ages unpicking it. My small judgement call is to open a separate bank account for the side hustle if it is doing anything meaningful. It does not have to be fancy. It just keeps the story clean if HMRC ever asks how you arrived at the numbers.

Look, this comes up a lot. Someone has been doing a bit of Uber Eats at weekends, selling on Etsy, or taking a few Fiverr jobs, and it simply did not click that it can need reporting. Especially if the money felt small month to month, or it was paid into the same bank account as everything else.

If you spot it now, that is a good thing. Correcting it sooner is usually better, because it keeps the numbers cleaner and it shows you are being straightforward.

What you do next depends on your situation. If you already file Self Assessment every year, you can often amend the return. Amending just means updating a tax return you have already submitted. If you do not normally file, the next step is usually to register for Self Assessment and submit a return for the year(s) affected.

If it goes back several years, or you are not sure which years are involved, you may be looking at a disclosure instead. A disclosure is basically you telling HMRC you have something to put right, and setting out the figures across the relevant years. In practice, it is calmer to do that in one organised go than to drip-feed corrections.

People also ask what HMRC letters look like. Often it is not dramatic. It tends to read like a nudge: we hold information that suggests you had income from X, please check your tax return, or please tell us if you need to declare something. Sometimes it asks you to review a specific tax year. Sometimes it is more general and points you to guidance.

On penalties, the important bit is that they depend on behaviour and timing. HMRC looks differently at a genuine mistake that you correct promptly versus something ignored after prompts. I am not going to throw numbers around here, but the direction of travel is simple: getting ahead of it usually helps.

A practical next step is to pull together your platform statements and bank transactions for each tax year (6 April to 5 April). Work out your total income and the key costs, then check whether you were over the £1,000 trading allowance. That allowance is a small tax-free amount for gross trading income, but once you are over it you usually need to report the whole activity, not just the excess.

One small judgement call from seeing this in real life: do not guess. If the figures are messy, take an extra hour to rebuild them from statements and receipts. A tidy, explainable set of numbers beats a quick estimate every time, especially if HMRC later asks how you arrived at it.

In practice, start with one simple number: roughly what was your gross side income for the tax year (6 April to 5 April). Gross just means the total that hit your account before costs. If you are on more than one platform, add them together. A bit of Deliveroo here, some eBay sales there, a couple of Fiverr jobs and an Airbnb weekend can look small on their own, but it adds up faster than people expect.

Once you have that estimate, compare it to the £1,000 trading allowance. If your total gross trading income is £1,000 or less, you are often in the “probably nothing to report” zone for that side hustle. Still keep basic records, because it is very easy to drift over the line next year without noticing.

If you are over £1,000, assume you need to declare it and move on to the next question: is it worth claiming your actual expenses instead of using the £1,000 allowance. You cannot usually have both. If your costs are low (say you do freelance work with very few expenses), the allowance can be simpler. If your costs are meaningful (delivery fuel, platform fees, materials, packaging, software subscriptions), claiming expenses can reduce the tax bill, but you need the paperwork to back it up.

Then check whether you already file Self Assessment. That is the yearly tax return system for people with income HMRC does not fully tax through payroll. If you already submit one for any reason (self-employed work, rental income, dividends, CIS, anything like that), the side hustle usually just becomes another set of figures to include. If you do not normally file, going over the allowance is often the point where you need to register and start.

Either way, keep records. Platform statements are good, but they do not always tell the whole story, and they can change format. Save the monthly summaries. Keep receipts for key costs. And do a quick quarterly check-in with yourself so you are not reconstructing a whole year from memory. My small judgement call: if you are close to the £1,000 mark, track it as you go rather than waiting until January. It saves a lot of stress for not much effort.

One more thing to keep in mind is how this sits with your other income. Side hustle profits do not live in a bubble. They stack on top of your job income, rental income, dividends, and anything else when HMRC looks at thresholds and reporting requirements, including Making Tax Digital (MTD). MTD is HMRC’s move towards more frequent digital reporting. If you have several income streams, or you are getting close to the MTD thresholds, it is usually worth getting advice early. Not because it is scary, but because it is easier to plan when you still have options.

If you would rather not guess, we can help you get this sorted properly. UK Tax Professionals is a small team. You deal with real people, not a ticket system. Vita and Kamile handle Self Assessment tax returns for side hustlers and small businesses, in plain language, so you know what is going on and why.

If you have never done one before, Self Assessment is just the yearly tax return where you tell HMRC about income that is not fully dealt with through PAYE (your normal payslip tax). Side hustle profits, platform income, rental income, and a few other bits often sit here.

We offer a free 30-60 minute consultation. It is usually a mix of tax planning (so you are not caught out), a look at your business structure (sole trader vs limited company, if that is relevant), and a quick check for missed deductions that people often forget about. No hard sell. Just a sensible steer on what to do next.

In practice, the most useful thing you can do before you call is pull together a rough total of what came in from each platform for the tax year, plus any obvious costs. Even a screenshot of monthly summaries is fine. My small judgement call: if you are over the £1,000 trading allowance, do not leave it until the rush. It is easier to fix when you still have time to find the records.

We are London-based, but we work with clients across the UK as well, so location is not a barrier.

You can reach us on 0792 1869 959 or email info@uktaxpro.co.uk. We are available Mon-Fri 9-5.

We often see people treat a side hustle as “just a bit extra” and then forget that HMRC can match what platforms report against what ends up on a tax return. One simple habit helps a lot in practice – keep a running total of your platform payouts as you go, rather than trying to rebuild it all at the end of the year.

My calm judgement call is this: if your combined side hustle income is nudging over the £1,000 trading allowance, or you are close to Making Tax Digital thresholds once you add property income, deal with it now and declare it properly. Most people are not doing anything dodgy, they are just busy, and small clean-ups are usually easier than a bigger tidy-up later.

If all of this still feels a bit much, or you just want someone to look at your numbers and tell you straight whether you need to worry about it – that’s literally what we do.

We handle the whole Making Tax Digital process for self-employed people and landlords.

Registration with HMRC, setting up your records (QuickBooks or a spreadsheet – either works), quarterly submissions, the end of year stuff, all of it. You don’t need to learn the system yourself.

First chat is free, no obligation, and a real person picks up the phone.

Here are other posts you may want to read.