If you have heard “Making Tax Digital” (or just “MTD”) and immediately thought “great, more tax” or “this is going to be an admin nightmare”, you are not alone. The thing is, MTD is not a new tax. It is a change to how you keep records and how you send information to HMRC. In plain English, HMRC wants you to keep your income and expenses in digital form, and send regular updates using software rather than typing it all in by hand at the end of the year.

This article is the simple overview. We will cover what MTD actually is, the phased start dates and income thresholds, why it is based on gross income (not profit, which catches people out), what “quarterly updates” really mean, and the basic software requirement. The step-by-step details and the “how do I do this in practice?” bits are in the other articles.

Making Tax Digital (MTD) is HMRC’s move to have you keep your business or property records digitally and send regular updates to them using compatible software.

The key point is that MTD is not a new tax. It does not create extra tax by itself. What it changes is how you record your income and expenses, and how you report figures to HMRC during the year. If you are used to saving receipts in a carrier bag and doing the tax return in one big push every January, this is the bit that needs a rethink.

HMRC is aiming MTD at self-employed people and landlords first. That includes lots of normal situations we see all the time: a subcontractor in construction, a tradesperson doing jobs on evenings and weekends, someone renting out a flat, or a side hustle selling on Etsy or taking bookings on Airbnb.

What stays the same is the part most people worry about. You still end up with an annual tax position and an annual tax bill, and the rules on what counts as income and what you can claim as expenses do not change just because you are using software. An “expense” still means a cost that is wholly and exclusively for the business, in plain words a genuine business cost.

In practice, the biggest shift is psychological. You move from “do it once a year” to “keep it ticking over”. My judgement call is to start getting your records into decent shape before you are forced to, even if you are under the threshold right now. The people who leave it late usually do not pay more tax, but they do end up stressed and scrambling for information that should have been tracked as they went along.

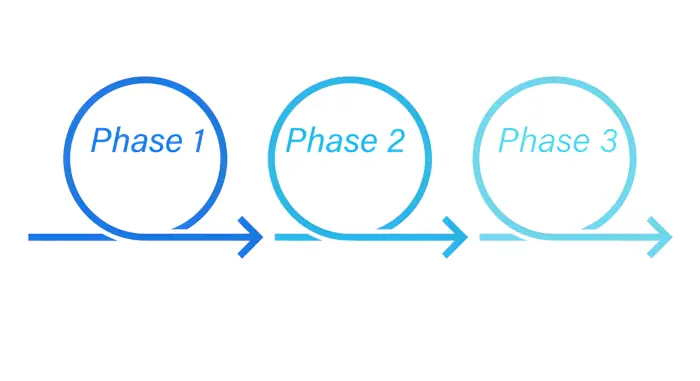

MTD for Income Tax (that is self-employed and landlords) is coming in three phases. Which phase you fall into is based on your annual income from self-employment and/or property. Not your profit. Income in this context means turnover for a business, or gross rent for landlords – before any expenses.

Phase 1 starts from April 2026 for people with gross income over £50,000. Phase 2 starts from April 2027 for people with gross income over £30,000. Phase 3 starts from April 2028 for people with gross income over £20,000.

The gross income point is the one that catches people out, to be honest. You can feel like a small business because you are not taking much home, but your turnover can still be high. Example: a subcontractor turns over £55,000 in the year, but spends £15,000 on materials, tools, van costs, insurance, and fuel. Their profit is £40,000, so they think they are under. But for MTD, the £55,000 turnover is what matters, so they are in from April 2026.

If you are under the threshold (for now), you generally stay on the current Self Assessment approach and do not have to join MTD yet. Practical tip – still get into the habit of keeping clean, up to date records. It makes the switch much less painful later, and it usually means fewer missed expenses along the way.

When HMRC talks about the MTD Income Tax thresholds, they are looking at income before expenses. That is gross income. Profit is what is left after you take off your business costs.

So, in plain English: gross income is the money coming in. Profit is the money you actually keep (before tax) once you have paid for things like materials, stock, fees, and repairs.

For most sole traders, “income” here basically means turnover. That is the total of your sales or invoices, before any costs. For landlords, it usually means your rental income. That is the gross rent you receive, before expenses like letting agent fees, repairs, and mortgage interest.

This is why people misjudge it. You can feel like you are not making much, because your costs are high. But the MTD threshold test is still looking at the bigger incoming number.

Example one: a construction subcontractor. Let’s say you invoice £60,000 over the year, but you spend a lot on materials and site costs, plus fuel and tools. You might only clear £35,000-£40,000 as profit. It still counts as £60,000 income for the MTD threshold.

Example two: a retailer with low margins. If you sell £80,000 of stock but most of that goes straight back out to suppliers, the profit might not look big. MTD is not judging how healthy the business is. It is just looking at the total sales figure going through the business.

Example three: a landlord. You might receive £36,000 a year in rent on a property, then have a big repairs year or high mortgage interest. The profit could be small, or even a loss. For the MTD threshold, the starting point is still the £36,000 gross rent.

If you are not sure where you sit, do not guess. Have a quick look at your last Self Assessment tax return. On the self-employed pages it will show your turnover, and on the property pages it will show your rental income. If you keep bookkeeping records, check your sales total and rent received for the tax year instead.

My small judgement call here: if you are hovering around a threshold, treat it like you are going to be pulled in soon and get your record keeping tighter now. It is calmer than doing the sums in a panic later, and it usually helps you keep on top of the business anyway.

Under MTD for Income Tax, you send HMRC a summary of your income and expenses four times a year, through software. Think of it like a quick snapshot of how the year is going so far, based on what you have recorded.

It is not four tax returns. It is not HMRC asking you to do your Self Assessment four times over. In practice, the quarterly updates are lighter touch. They are totals, not the full detail and not the final word on your tax position.

It also does not automatically mean you will be paying tax four times a year. For most people, tax is still settled through the usual process, and the quarterly updates are about reporting, not collecting.

There is still an end-of-year finalisation step. That is where you confirm the figures for the whole tax year, make any accounting adjustments, and add anything else that belongs on your tax return. In plain English, the quarterly updates are the running totals, and finalisation is where you tie it all down properly.

The useful bit to remember is this: the updates are only as good as your records. If your bookkeeping is messy, you will be sending messy numbers. If you have missed invoices, not logged cash takings, or mixed personal and business spending, the update will reflect that.

A practical approach that works for a lot of small businesses is to set a simple rhythm. Keep on top of your sales and main costs monthly, and do a quick tidy-up before each quarterly update is due. My judgement call here: do not aim for perfection each quarter. Aim for “complete and sensible”. Save the heavy clean-up for the year end, when it actually matters.

For MTD for Income Tax, you will need MTD-compatible software to do two things: keep your business records in a digital form, and send the quarterly updates to HMRC.

When HMRC says “digital records”, they mean your income and expenses are recorded in software, not just on paper or as loose notes. It does not have to be complicated. It just needs to be stored in a way the software can use to produce the totals for each quarter.

In practice, most people end up in one of two camps. Either you use accounting software (where you log sales and costs as you go), or you use a spreadsheet and then use bridging software to submit the quarterly update. Bridging software is simply a tool that takes the figures from your spreadsheet and sends them to HMRC in the right format.

A quick reality check, because this catches people out. The method will not be “type the totals into HMRC’s website” like some people do now. And it will not be sending screenshots, PDFs, or photos of your spreadsheet. The submission has to go through compatible software.

If you are already using software for invoicing, bookkeeping, or VAT, this might be more of a setup and habit change than a full overhaul. You may just need to make sure the right business is set up, the categories make sense, and you have a routine for keeping it updated so quarterly reporting is not a scramble.

The day-to-day part is usually the real shift. You need to get comfortable recording things as you go, or at least monthly, rather than trying to rebuild the year from bank statements at the end. My small judgement call: if you are currently a “shoebox and a weekend in January” person, pick a simple system now and practise with it before MTD forces the issue. It is much less painful.

Most people do not need to become MTD experts. You just need to know which side of the line you are on, and what changes once you cross it.

If you are a CIS subcontractor (CIS is the construction scheme where contractors take tax off your payments), this matters because your income can look “high” even when your take-home feels average. Same if you do deliveries for Uber Eats, sell on Etsy, or have a side hustle alongside a PAYE job. The totals add up quicker than you think.

Landlords are another common one. Even with one or two properties, your gross rental income (the rent coming in, before costs) can push you over a threshold. It is not about profit. It is about the total income you receive.

Partnerships need a quick sense check too. A small partnership can be two people doing good, steady work, and the gross income can cross the line even when each partner’s share of profit is modest. If you are not sure what counts as “partnership income”, think of it as the partnership’s business income before it is split between the partners.

Here is the practical checklist in plain English. First, work out your gross income for the relevant tax year from self-employment and/or property. Gross means before expenses. If that total is over the threshold for the phase you fall into, then from your MTD start date you will need to keep digital records, use compatible software, and send quarterly updates.

If you are under the threshold, you can breathe for a bit. But it is still worth getting your bookkeeping more digital, because it makes everything easier anyway. Fewer missing receipts. Less guesswork at tax return time. And if your income jumps in a busy year, you are not starting from scratch.

In practice, the people who feel least stressed are the ones who do a small amount early. Pick a simple method and get into a monthly habit. My judgement call: even if you are not sure you will be in the first wave, set up the software or spreadsheet routine now while there is no deadline breathing down your neck.

Leaving it until the last minute does not make you a bad taxpayer. We see it all the time. It just makes the first few submissions more frantic than they need to be, because you are learning the system and fixing the records at the same time.

First, pull together last year’s figures and do a quick sense check on where you sit. You are looking for gross income, not profit – so turnover from self-employment plus rental income, before expenses. This is the bit that catches people out, especially if you have big materials costs, CIS deductions, or you are juggling a couple of income streams.

Next, pick a simple record-keeping routine you can actually stick to. Weekly works well if you have lots of small transactions (retail, Etsy, food delivery). Monthly is fine for many trades and landlords, as long as you do it every month and do not let it slide. My judgement call: choose the slower option you will keep doing. Consistency beats a perfect system you abandon.

Then think about how you are going to keep those records. If you are already using bookkeeping software, you may just need to tidy up your categories and make sure you are reconciling the bank properly. If you are using a spreadsheet, that can still work, but you may need bridging software – that is a tool that takes your spreadsheet totals and submits the MTD updates to HMRC in the right format.

If you want, give us a call or drop us an email and we will talk it through. We can help you work out which phase applies, whether your gross income puts you over the line, and what setup makes sense for how you actually run things. And yes, a real person answers the phone. You can reach us on 0792 1869 959 or info@uktaxpro.co.uk.

We often see people get caught out by the gross income test, especially when they have high costs and they are thinking in profit terms. One practical habit that helps is to review your record-keeping once a month, not at the year end, and make sure every sale and rent payment is actually captured.

If you are anywhere near the threshold, treat MTD 2026 like a change in routine rather than a big event. In practice, getting your numbers into a regular rhythm early makes the quarterly updates feel like a quick check-in, instead of a stressful scramble.

If all of this still feels a bit much, or you just want someone to look at your numbers and tell you straight whether you need to worry about it – that’s literally what we do.

We handle the whole Making Tax Digital process for self-employed people and landlords.

Registration with HMRC, setting up your records (QuickBooks or a spreadsheet – either works), quarterly submissions, the end of year stuff, all of it. You don’t need to learn the system yourself.

First chat is free, no obligation, and a real person picks up the phone.

Here are other posts you may want to read.